Opportunities for Insurers Within a Shifting Credit Cycle

By Matthew Daly, CFA, Managing Director and Head of Corporate and Municipal Teams

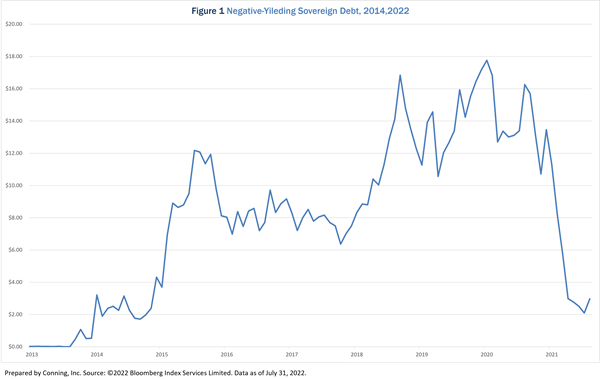

Monetary policy around the world is changing as many central banks are attempting to tighten financial conditions in order to control rampant inflation. As illustrated in Figure 1, negative-yielding sovereign debt has seen a nearly 10-fold decline across the globe.

The tightening has generated recession fears and market volatility and contributed to wider corporate spreads. There are concerns that the Fed, in an effort to squelch inflation, will ultimately destroy demand and trigger a recession. Indeed, with two consecutive quarters of GDP contraction in 2022, it appears the economy has, at a minimum, slowed meaningfully. While corporate fundamentals are currently on solid ground, investors are weighing the impact of a possible recession on the corporate market.

Despite the macro uncertainty, Conning believes opportunities can be uncovered by applying strong analytical skills and investment discipline as well as by leveraging our deep experience in managing through market cycles. While the months ahead should feature higher volatility, they should also present distinctive opportunities as yields are at some of the highest levels in a decade.

We see potential in issuers with durable credit fundamentals that can weather an economic downturn while keeping their credit profiles largely intact. Additionally, securities that were issued recently when interest rates were lower and credit spreads tighter are now available at a meaningful discount to par. Many may be opportunities for longer-term investors - such as insurers - who can hold them to maturity.

Fundamentals: Holding Up but Pressure Mounting

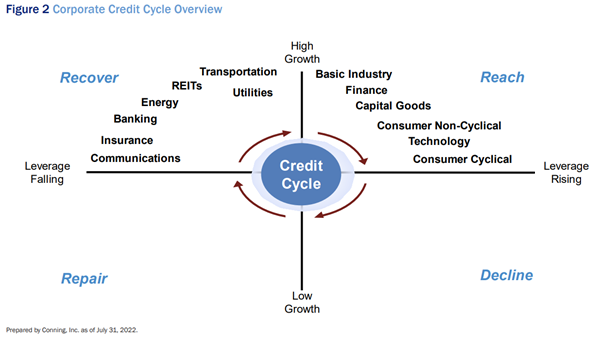

The slowing economy and rising concerns of recession contribute to Conning’s belief that the corporate market is moving into the later stages of the credit cycle (see Figure 2).

Click below to continue reading Conning’s Viewpoint, “Opportunities for Insurers Within a Shifting Credit Cycle."

Risks

Market Risk - Market, or systematic, risk is the risk that individual securities may be correlated with general market downturns regardless of the particular business conditions and outlook for the individual companies.

Credit Risk – eroding fiscal health in issuing companies resulting in inability to meet debt obligations.

Inflation Risk - Inflation erodes the purchasing power of future cash flows from investments. In times of high inflation the value of securities may be reduced.

Liquidity Risk - Liquidity risk can occur when market conditions do not allow transactions to be made in a quick and orderly fashion in relation to indicative market prices.

©2022 Conning, Inc. All rights reserved. The information herein is proprietary to Conning, and represents the opinion of Conning. No part of the information above may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system or translated into any language in any form by any means without the prior written permission of Conning. This publication is intended only to inform readers about general developments of interest and does not constitute investment advice. The information contained herein is not guaranteed to be complete or accurate and Conning cannot be held liable for any errors in or any reliance upon this information. Any opinions contained herein are subject to change without notice. These materials contain forward-looking statements. Investors should not place undue reliance on forward-looking statements. Actual results could differ materially from those referenced in forward-looking statements for many reasons. Forward-lookingstatements are necessarily speculative in nature, and it can be expected that some or all of the assumptions underlying any forward-looking statements will not materialize or will vary significantly from actual results. Variations of assumptions and results may be material. Without limiting the generality of the foregoing, the inclusion of forward-looking statements herein should not be regarded as a representation by the Investment Manager or any of their respective affiliates or any other person of the results that will actually be achieved as presented. None of the foregoing persons has any obligation to update or otherwise revise any forward-looking statements, including any revision to reflect changes in any circumstances arising after the date hereof relating to any assumptions or otherwise. Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC and Global Evolution Holding ApS and its group of companies are all direct or indirect subsidiaries of Conning Holdings Limited (collectively “Conning”) which is one of the family of companies owned by Cathay Financial Holding Co., Ltd. a Taiwan-based company. C# 15622617