Rising Inflation: What’s the MPL Industry to Do?

“Get Ready for the Great U.S. Inflation Mirage of 2021” —Bloomberg Quint, December 7, 2020

“U.S. Inflation Hit 7% in December, Fastest Pace Since 1982” —Wall Street Journal, January 12, 2022

By Bill Burns, a Director in Insurance Research, and Lauryn Kothavale, an Assistant Vice President in Insurance Research

Heading into 2021, projections for U.S. inflation were mixed. At least two economists were on record saying “2021 will be a year plagued by numerous unwarranted inflation scares.” For the first three months of 2021, this outlook seemed reasonable with consumer price index inflation averaging approximately 1.9%. Then, in April 2021, CPI inflation jumped to 4.2%, climbed steadily for the rest of the year. In December, inflation eventually reached a high for the year of 7.0%.1

The last time CPI inflation exceeded 6% was back in the late 1970s/early 1980s. Inflation during that period was partly due to surges in the price of oil, while measures taken to curtail inflation included wage and price freezes, surcharges on imports, and a break with the gold standard. At the time, the Federal Reserve implemented tight monetary policies that raised the federal funds

rate from 10% to 20%. While these actions resulted in a recession, the policy proved effective and in 1982 the trend of high inflation subsided.

Various reasons are given for the current spike in inflation including supply bottlenecks, government policy, pent-up consumer demand for goods, imbalances in supply and demand, and a lack of competition among corporations. Government stimulus spending since the pandemic has exceeded $5 trillion. Congress and the White House are still discussing additional stimulus spending. Continued availability of disposable income and hampered supply chains are expected to contribute to ongoing inflationary pressures well into 2022.

Not All Inflation Is Created Equal

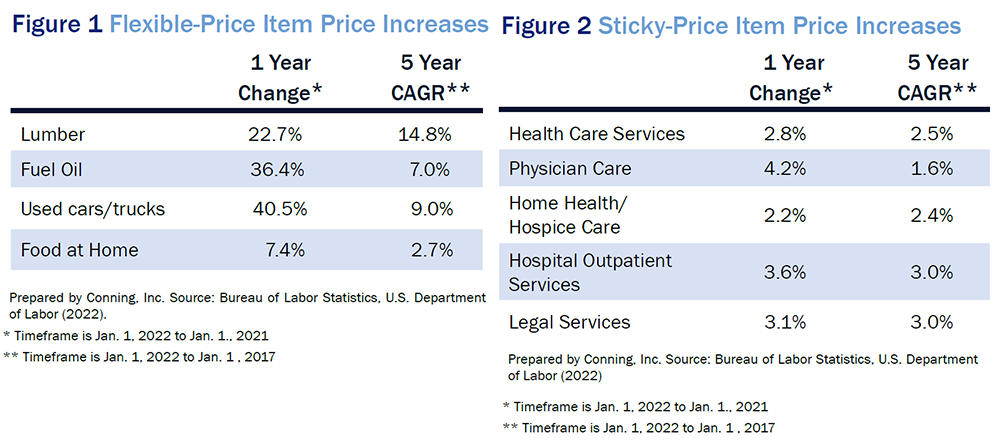

If the price changes for a particular CPI component occur less often--on average--than every 4.3 months, that component is called a “sticky-price” good. Goods that change prices more frequently are labeled “flexible-price” goods. Examples of sticky-price goods are medical care services, education, public transportation, and motor vehicle maintenance. Examples of flexible-price goods arelumber, fuel oil, used cars/trucks, and food at home.

As shown in Figures 1 and 2, most of the headline inflation during 2021 has come from price increases for flexible goods. Sticky-price goods—many of which underlie liability claim costs—have been lower than headline inflation.

Click below to continue reading Conning’s Viewpoint, “Rising Inflation: What's the MPL Industry to Do?."

Disclosure

©2022 Conning, Inc. All rights reserved. The information herein is proprietary to Conning, and represents the opinion of Conning. No part of the information above may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system or translated into any language in any form by any means without the prior written permission of Conning. This publication is intended only to inform readers about general developments of interest and does not constitute investment advice. The information contained herein is not guaranteed to be complete or accurate and Conning cannot be held liable for any errors in or any reliance upon this information. Any opinions contained herein are subject to change without notice. Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Advisors, LLC and Global Evolution Holding ApS and its group of companies are all direct or indirect subsidiaries of Conning Holdings Limited (collectively “Conning”) which is one of the family of companies owned by Cathay Financial Holding Co., Ltd. a Taiwan-based company. C# 14955958