March 07, 2024

Esoteric ABS: Opportunities for Yield and Portfolio Diversification Amid Market Volatility

Samantha Andreoli, a Director in Conning’s Business Development unit, spoke with Mike Nowakowski, a Managing Director and Head of Structured Products at Conning, about market conditions and opportunities in esoteric asset-backed securities (ABS).

- Samantha: Insurers are familiar with ABS as they have been common allocations for insurance company portfolios for many years. But what exactly is “esoteric ABS”?

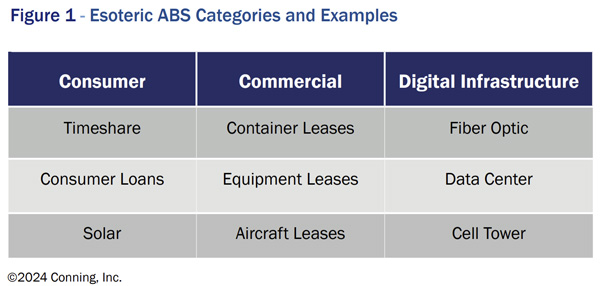

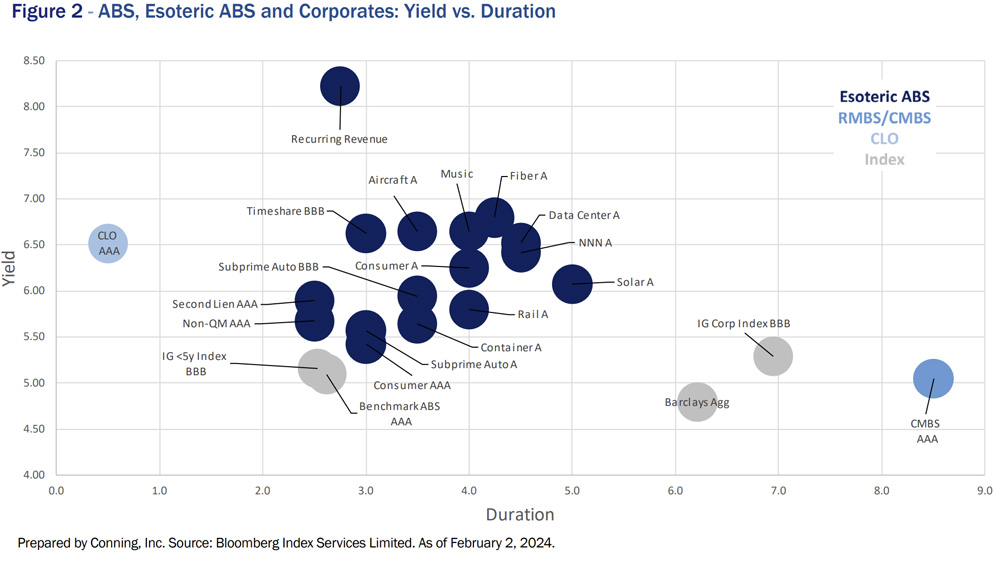

Mike: The ABS subset known as esoteric ABS is very similar to traditional auto and credit card ABS, but the collateral may be less familiar. Most esoteric ABS deals can be divided into three large categories: consumer, commercial, and digital infrastructure (see examples in Figure 1). Esoteric ABS currently offers yields at a premium to traditional ABS (see Figure 2) as well as other assets of similar quality and duration. The asset class features strong liquidity and may improve portfolio diversification, valuable attributes for insurers. While not as well-known as more traditional ABS collateral such as credit card receivables, esoteric collateral has a great deal of information available for analysts to study. Gathering and formatting the data may take additional work but it may be worth the potential reward.

- What are the diversification and yield/spread benefits that esoteric ABS offers insurers?

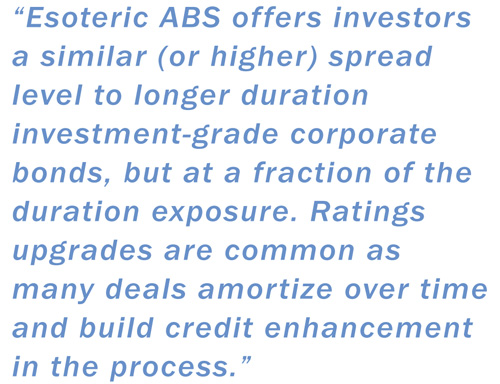

Rotation into structured products is a theme that we’ve seen since the pandemic as investors diversify into options that offer structural protections with shorter duration. Esoteric ABS offers investors a similar (or higher) spread level to longer duration investment-grade corporate bonds, but at a fraction of the duration exposure. Rating upgrades are common as many deals amortize over time and build credit enhancement in the process.

Not only is esoteric ABS a good diversifier from an investment product perspective, but within the asset class it offers a diverse set of collateral options including prime consumer, subprime consumer, the shipping industry, construction equipment, digital infrastructure and others.

- Why is esoteric ABS a good complement for insurers’ existing structured / CLO allocations?

Collateralized loan obligations (CLOs), as a function of their floating-rate nature, have been stand-out performers in fixed income since the U.S. Federal Reserve (the Fed) began hiking monetary policy rates in 2022. With the Fed seemingly ready to transition again to a less restrictive stance, rate cuts are widely expected in 2024. We think from both a spread-tightening perspective as well as a fixed-rate, duration-additive perspective, esoteric ABS will serve a useful purpose for insurers’ portfolio allocations going forward. Adding fixed-rate duration on the front end of the curve in an environment where the Fed is poised to cut rates should be a good complement to a CLO allocation.

- How is the current interest rate environment affecting esoteric ABS?

Performance for esoteric ABS was challenged in 2022 as the Fed embarked on an aggressive rate hiking campaign and spreads widened into the broader risk-off environment. Consequently, the inverted nature of the Treasury curve at present makes the front-end of the duration spectrum very attractive. Add wider spreads on top of that, and esoteric ABS offers a very attractive entry point and an appealing yield per unit of duration. As the Fed pivots to reducing the restrictive nature of monetary policy, shorter fixed-rate duration should benefit as the curve steepens.

- What other market dynamics are affecting the esoteric ABS asset class?

Of the many dynamics in the market, two are commanding a lot of our attention. One is the Red Sea conflict, which has global ramifications for the shipping industry. Container ships are rerouting around the Horn of Africa, adding 20-30% to travel time, which is causing shipping rates to reprice significantly higher. This is a challenge for the shipping industry but it’s great for container lessors (who issue ABS deals) because operators will need more containers and more container ships to make up for the delay of deliveries. As a result, container utilization and demand will rise, improving the fundamentals of container deals.

The second dynamic concerns the aircraft industry which has also been in the headlines, but when we think about lessors in the space we are optimistic. There is a global shortage of aircraft, particularly engines, now that air and passenger traffic is back to pre-pandemic levels. We think narrowbody aircraft and engine lease transactions offer solid fundamentals and typically come at very attractive spread levels.

- What has changed in the asset class since the 2008-2009 financial crisis?

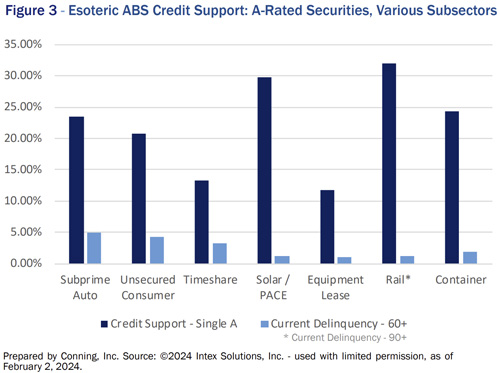

When most of us think of the deals of that era that experienced heavy losses, we think of over-levered consumers with subprime mortgages at high debt-to-income ratios. But esoteric ABS is very different from legacy residential mortgage-backed securities (RMBS) products. For starters, the collateral backing esoteric ABS deals is not mortgage related. In addition, the underwriting process has become more efficient and lenders have done a much better job at managing the risk within their respective credit boxes. Lastly, and arguably most importantly, the structural protections in esoteric ABS deals issued after the financial crisis have higher levels of credit enhancement. Levels of credit enhancement at the single-A level across various subsectors more than account for the level of 60+ day delinquencies we are experiencing in the market currently. Even if all those delinquencies came through as defaults, there would be sufficient credit enhancement to enable these tranches to continue to pay principal and interest to investors (see Figure 3).

- What are you watching in 2024 that you think could affect esoteric ABS?

Two items on our radar are the evolution of the U.S. consumer and the rise of digital infrastructure and artificial intelligence (AI). The health of the consumer has been a big topic of conversation during the past 18 months, but we think it is more nuanced than the U.S. consumer en masse; data show that it has been a story of the prime consumer versus the subprime consumer. The prime, homeowning consumer has enjoyed rising home prices and equity markets as well as an increase in wages. As a result, delinquencies for prime-related ABS collateral have been well contained. On the other hand, we have seen rising delinquencies above 2008-09 levels for subprime auto and unsecured consumer loans as inflation has affected the lower-FICO-score, paycheck-to-paycheck borrowers to a greater extent. We do, however, feel that we are approaching an inflection point in delinquencies and expect better consumer metrics into 2024.

The recent rise in AI has led corporations and individuals to demand greater computing power. This has led to an increase in corporate capital expenditures in digital infrastructure. As a result, we have seen significant growth in digital infrastructure-related ABS in the form of data center and fiber network deals. Data centers offer cashflows backed by the leases on the center’s tenants, which can vary by scale in the form of colocation, wholesale and hyperscale. Additionally, we have seen several fiber-optic network ABS deals. As the need for computing power (and more importantly, space) expands, we feel that growth and subsequent issuer tiering in this sector will continue to develop.

- How do you stress test portfolios and what market trends are you monitoring?

We have a robust modeling and surveillance process from both a macro top-down and bottom-up perspective. Every month, our Risk department holds an Investment Risk Committee meeting to discuss and highlight key metrics about overall firm positioning. We also flag any outsized risks in the portfolio that surface based on economic and market scenario modeling.

On a more micro basis, we run an automated monthly process that takes data from several inputs for each deal (and tranche) we own. The system consolidates the data and important up-to-date deal metrics into a view where we can see changes in deal performance month-over-month. This will give us an early view into how delinquencies, defaults, loss coverage ratios, and overall subsector health are evolving. We can know on a tranche-by-tranche basis where the potholes might emerge or conversely where we should focus more capital.

The trends we’ve seen recently are similar to what I mentioned earlier: the rise in subprime borrower delinquencies has been more rapid than those of prime consumers. Another trend we are seeing is strong commercial collateral deal performance: container deals are delivering nicely and building credit enhancement, small and medium-sized-ticket equipment performance is stable with very low losses - less than 1%.

Overall, we are comfortable with the direction of the consumer (especially prime borrowers) as well as what we are seeing in commercial. With borrowing rates poised to come down this year, we anticipate a good year of issuance in the ABS space and are optimistic on fundamentals.

|

Mike Nowakowski is a Managing Director and Head of Structured Products, responsible for overseeing the structured research and trading team. Prior to joining Conning in 2022, he was a portfolio manager focused on Agency MBS and ABS at GE Asset Management, State Street Global Advisors, and most recently People’s United Bank. Previously, Mr. Nowakowski was a portfolio manager focused on Money Markets. Mr. Nowakowski earned a bachelor’s degree in business and graduated Magna Cum Laude from Plymouth State University. |

|

Samantha Andreoli is a Director in Business Development. Prior to joining Conning in 2023, she was a Vice President of Business Development & Investor Relations with Shenkman Capital Management. She began her career at Conning in Business Development. Ms. Andreoli earned a bachelor of arts degree from the University of Connecticut. |

ABOUT CONNING

Conning (www.conning.com) is a leading investment management firm with a long history of serving the insurance industry. Conning supports institutional investors, including insurers and pension plans, with investment solutions, risk modeling software, and industry research. Founded in 1912, Conning has investment centers in Asia, Europe and North America

Esoteric ABS Risk Factors

Investment Risk - The potentially complex structure of the security may produce unexpected investment results not based on default or recovery statistic.

Valuation Risk - Valuation of structured credit products are provided by third parties, based on models, indicative quotes, and estimates of value, in addition to historical trades. There is inherent difficulty in valuing these assets, and there can be no assurances the assets can be disposed of or liquidated at the valuations established, or that published returns will be achieved.

Underlying Asset Credit Risk - During periods of economic uncertainty and recession, the incidence of modifications and restructurings of investments may increase, resulting in impairments to the underlying asset value.

Economic Risk - Changing economic, political, regulatory or market conditions, interest rates, general levels of economic activity, the price of securities and debt instruments and participation by other investors in financial markets may affect the value of the structured security and all other asset classes.

Additional Source Information:

Bloomberg Index Services Limited. Used with permission. Bloomberg is a trademark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg does not approve this material, guaranty the accuracy of any information herein, or make any warranty as to the results to be obtained therefrom, and shall not have any liability for injury or damages arising in connection therewith.

Disclosures

Past performance is not a guarantee of future results.

©2024 Conning, Inc. This document and the software described within are copyrighted with all rights reserved. No part of this document may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of Conning. Conning does not make any warranties, express or implied, in this document. In no event shall Conning be liable for damages of any kind arising out of the use of this document or the information contained within it. This document is not intended to be complete, and we do not guarantee its accuracy. Any opinion expressed in this document is subject to change at any time without notice.

This document contains information that is confidential or proprietary to Conning (or their direct or indirect subsidiaries). By accepting this document you agree that: (1) if there is any pre-existing contract containing disclosure and use restrictions between your company and Conning, you and your company will use the information in this document in reliance on and subject to the terms of any such pre-existing contract; or (2) if there is no contractual relationship between you and your company and Conning, you and your company agree to protect the information in this document and not to reproduce, disclose or use the information in any way, except as may be required by law.

ADVISE ®, FIRM ®, GEMS ®, CONNING CLIMATE RISK ANALYZER ® and CONNING ALLOCATION OPTIMIZER ® are registered trademarks of Conning, Inc. in the U.S. Copyright 1990-2024 Conning, Inc. All rights reserved. ADVISE ®, FIRM ®, GEMS ®, CONNING CLIMATE RISK ANALYZER ® and CONNING ALLOCATION OPTIMIZER ® are proprietary software published and owned by Conning, Inc.

This document is for informational purposes only and should not be interpreted as an offer to sell, or a solicitation or recommendation of an offer to buy any security, product or service, or retain Conning for investment advisory services. The information in this document is not intended to be nor should it be used as investment advice.

C: 17937943