February 28, 2022

Esoteric ABS Q&A: Potential Relative Value During Market Disruptions

Conning’s Head of Consultant Relations, David Motill, spoke with Paul Norris, Head of Structured Products for Conning, about market conditions that are creating opportunities in esoteric asset-backed securities (ABS).

- David: Why should insurers consider esoteric ABS?

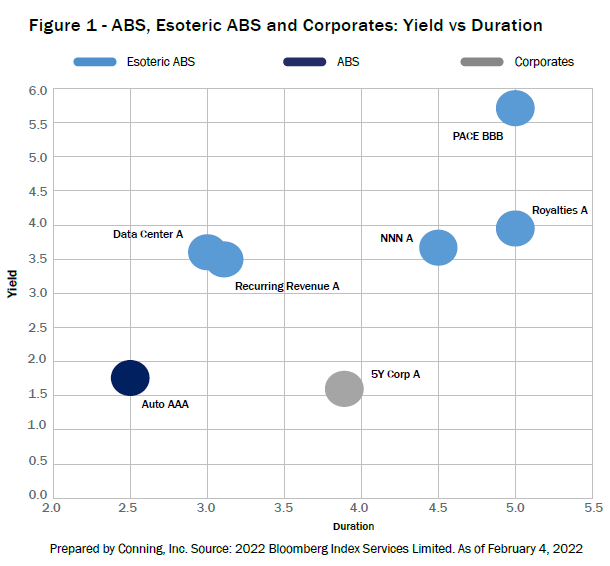

Paul: The ABS subset known as esoteric ABS may be less familiar to investors, but it currently offers yields at a premium to traditional ABS (see Figure 1) as well as other assets of similar quality and duration. The asset class features strong liquidity and may improve portfolio diversification, valuable attributes to insurers as we enter a period of potentially higher volatility.

Most esoteric ABS are backed by collateral such as commercial aircraft, railcars and shipping containers. While not as well-known as more traditional ABS collateral such as credit card receipts, esoteric collateral has a great deal of information available for analysts to study. Gathering and formatting the data may take additional work but it may be worth the potential reward.

- What impact will the Biden infrastructure bill have on esoteric ABS?

Conning believes the federal infrastructure bill signed into law in November 2021 will have a positive impact on the esoteric ABS market. The bill calls for spending $1 trillion to upgrade outdated roads, bridges, transit systems and more during the next 10 years and that is good news for esoteric ABS collateral. Conning believes the spending will drive a need for equipment, increase demand for transporting various materials via railroad cars, and generate growth that should benefit subsectors like unsecured consumer loans.

We expect some subsectors will see early rewards from this spending.

Equipment leases will likely benefit from the immense need for equipment - both big ticket and small - to fix the one in five miles of U.S. highways and major roads deemed to be in poor condition. The bill has $40 billion alone dedicated to repairing some 45,000 bridges.1

Related to that repair work, we think rental car fleet leases will also benefit. The contractors and firms - construction, engineering, etc. – that win contracts will need to get their people to job sites. We also think these conditions bode well for rail car leases given strong demand to transport the materials needed to complete these jobs, such as steel and other metals, rare earths, equipment and energy. We expect rail to be the preferred mode of transportation based on its efficiency and scale.

We think the bill will also benefit other esoteric ABS subsectors.

For example, data centers should benefit from the $65 billion earmarked to provide broadband internet access to all Americans. More than 30 million Americans live in areas with no broadband internet access,1 and this expansion should also help lower the price for broadband. Currently, the U.S. has the second-highest broadband costs of the 35 OECD countries.2

An improved power grid, increased broadband access and enhanced worker productivity should benefit the U.S. technology sector and thus recurring revenue and venture debt.

The legislation also calls for investing $25 billion in U.S. airports, and improvements in airport infrastructure should ultimately support greater passenger volume and thus aircraft ABS.1

- Do esoteric ABS offer investors an inflation hedge?

While inflation is expected to persist through 2022, investors may appreciate that esoteric ABS can be an inflation hedge. Specific subsectors such as container, triple net lease, aircraft and rail have leases on physical property, which may benefit from inflation in several ways.

First, rising prices cause increases in property value, thus reducing ABS residual risk on the assets. Second, inflation allows for increases in leasing rates, thus increasing cash flow to service the fixed-rate debt during the investment term. For example, some subsectors, such as triple net lease, have annual rent adjustments based on CPI resulting in yearly cash flow increases, reducing ABS credit risk.

Finally, many esoteric ABS securities are floating rate or have short maturities which limit the impact of rising rates on the assets.

- How have supply chain issues affected esoteric ABS collateral?

There has been significant progress made in reducing port congestion. According to the Marine Exchange of Southern California, there were 34 ships within 25 miles of Los Angeles/Long Beach waiting to unload as of February 7, and 92 total in that zone when you include those loading and/or unloading cargo. This is a significant improvement versus the peak back on November 16, when there were 179 ships inside that 25-mile zone, with 114 of them simply waiting. The 34 ships currently waiting also compares favorably to the pre-COVID peak of 48 in 2014 and 2015.

The time to move a container thru the port, known as the “dwell time,” has been reduced by more than half since the supply disruption peak. For example, according to the Port of

L.A. Operations Report, the dwell times for containers at the port are now five days versus a peak of 11 based on a trailing 30-day basis as of February 8.

While various factors have led to the supply chain disruption during the pandemic, container ports in critical global markets have been the epicenter of the issue due to congestion and rolling COVID lockdowns.

Record consumer demand for foreign goods during the pandemic combined with labor shortages within the transportation sector led to congestion and a buildup of container boxes in the wrong locations. This slows the velocity of containers moving to where they are needed globally.

The transportation worker shortage has also impacted port congestion. For example, the American Trucking Association estimates a shortage of 80,000 drivers, an all-time high.3 The employment shortage also applies to rail, the other primary way of transporting containers once they reach port. The number of workers on Class I freight railroads is estimated to be down about 20% from 2017 (170,000 in 2017 versus 135,000 currently).4

- Can investors find Environmental, Social, Governance (ESG) opportunities in esoteric ABS?

A significant portion of the available green/ESG bonds can be found in esoteric ABS. According to Conning’s analysis, esoteric green bonds represent approximately $14 billion in outstanding transactions, with the majority ($10 billion) in solar/PACE but other subsectors such as rail and even data centers are represented as well.

Rail ABS offer investments in efficient goods transportation with a reduced climate impact. U.S. railroads can move one ton of freight more than 480 miles on just one gallon of fuel, and while railroads account for 40% of U.S. long-distance freight volumes - more than any other form of transport - they generate only 1.9% of U.S. transportation-related greenhouse gases.5 Trinity Rail, the dominant ABS issuer, has created a green financing framework in accordance with the 2018 Green Bond Principles set out by the ICMA, LMA, APLMA, and LSTA. Trinity’s entire $3.3 billion of ABS securities outstanding are rated “Green Bonds.”

Paul Norris is a Managing Director and Head of Structured Products and oversees the team involved in the research and trading of structured securities. Prior to joining Conning in 2017, he was a hedge fund portfolio manager focused on mortgage derivatives. Previously, Mr. Norris was head of securitized products at Dwight Asset Management, where he led a team of portfolio managers, traders and analysts, and also has served as director of mortgage and non-mortgage investments at Fannie Mae. Mr. Norris earned a BS in finance from Towson University and an MBA from the University of Maryland.

David D. Motill is a Managing Director and Head of Consultant Relations at Conning. Prior to joining the firm in 2010, Mr. Motill was a partner and chief marketing officer at Alpha Equity Management. He previously headed consultant relations groups with Fischer Francis Trees & Watts, Citigroup Asset Management and GE Asset Management. Mr. Motill earned a degree from Temple University and an MBA from the University of Notre Dame and holds Series 7 and 63 licenses.

ABOUT CONNING

Conning (www.conning.com) is a leading investment management firm with a long history of serving the insurance industry. Conning supports institutional investors, including insurers and pension plans, with investment solutions, risk modeling software, and industry research. Founded in 1912, Conning has investment centers in Asia, Europe and North America.

Esoteric ABS Risk Factors

Investment Risk - The potentially complex structure of the security may produce unexpected investment results not based on default or recovery statistic.

Valuation Risk - Valuation of structured credit products are provided by third parties, based on models, indicative quotes, and estimates of value, in addition to historical trades. There is inherent difficulty in valuing these assets, and there can be no assurances the assets can be disposed of or liquidated at the valuations established, or that published returns will be achieved.

Underlying Asset Credit Risk - During periods of economic uncertainty and recession, the incidence of modifications and restructurings of investments may increase, resulting in impairments to the underlying asset value.

Economic Risk - Changing economic, political, regulatory or market conditions, interest rates, general levels of economic activity, the price of securities and debt instruments and participation by other investors in financial markets may affect the value of the structured security and all other asset classes.

Footnotes:

1. The White House, “Fact Sheet: The Bipartisan Infrastructure Deal,” Nov. 6, 2021, https://www.whitehouse.gov/briefing-room/statements-releases/2021/11/06/fact-sheet-the-bipartisan-infrastructure-deal/

2. Broadbandsearch.net, “How Do U.S. Internet Costs Compare to the Rest of the World,” https://www.broadbandsearch.net/blog/internet-costs-compared-worldwide

3. American Trucking Association press release, “ATA Chief Economist Pegs Driver Shortage at Historic High,” Oct. 25, 2021, https://www.trucking.org/news-insights/ata-chief-economist-pegs-driver-shortage-historic-high

4. Statista.com, “Number of employees in U.S. freight rail industry from 2014 to 2020,” https://www.statista.com/statistics/562887/us-class-onerailroads-number-of-employees/

5. FreightWaves.com, “Daily Infographic: Railroads: Eco Friendly,” July 12, 2021; https://www.freightwaves.com/news/daily-infographic-railroads-eco-friendly

Additional Source Information:

Bloomberg Index Services Limited. Used with permission. Bloomberg is a trademark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg does not approve this material, guaranty the accuracy of any information herein, or make any warranty as to the results to be obtained therefrom, and shall not have any liability for injury or damages arising in connection therewith.

Disclosures

Past performance is not a guarantee of future results.

These materials contain forward-looking statements. Investors should not place undue reliance on forward-looking statements. Actual results could differ materially from those referenced in forward-looking statements for many reasons. Forward-looking statements are necessarily speculative in nature, and it can be expected that some or all of the assumptions underlying any forward-looking statements will not materialize or will vary significantly from actual results. Variations of assumptions and results may be material. Without limiting the generality of the foregoing, the inclusion of forward-looking statements herein should not be regarded as a representation by the Investment Manager or any of their respective affiliates or any other person of the results that will actually be achieved as presented. None of the foregoing persons has any obligation to update or otherwise revise any forward-looking statements, including any revision to reflect changes in any circumstances arising after the date hereof relating to any assumptions or otherwise.

©2022 Conning, Inc. All rights reserved. The information herein is proprietary to Conning, and represents the opinion of Conning. No part of the information above may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system or translated into any language in any form by any means without the prior written permission of Conning. This publication is intended only to inform readers about general developments of interest and does not constitute investment advice. The information contained herein is not guaranteed to be complete or accurate and Conning cannot be held liable for any errors in or any reliance upon this information. Any opinions contained herein are subject to change without notice.

Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Advisors, LLC and Global Evolution Holding ApS and its group of companies are all direct or indirect subsidiaries of Conning Holdings Limited (collectively “Conning”) which is one of the family of companies owned by Cathay Financial Holding Co., Ltd. a Taiwan-based company.

C: 14514978